Choosing the Right Business Entity in California: LLC, Partnership, or Corporation - Tax Considerations

When starting or restructuring a business in California, choice of legal entity is a critical decision that impacts taxation, management, and overall operations. The most common options include partnerships (both general or limited), limited liability companies (“LLCs”), and corporations (C-corporations or S-corporations). For the most part, California conforms with the U.S. federal income tax treatment of these entities but some differences do exist.

Overview of Business Entities in California

Partnerships: These include general partnerships (GPs), where two or more individuals share ownership and operations, and limited partnerships (LPs), which have general partners who manage the business and limited partners who primarily invest. A joint venture is also a form of partnership.

Limited Liability Companies (LLCs): A hybrid entity combining elements of partnerships and corporations, offering flexibility in taxation and management.

Corporations: Divided into C-corporations (standard corporate taxation) and S-corporations (pass-through taxation with restrictions), both providing a formal structure separate from owners.

All entities (including joint ventures) doing business in California must register with the California Secretary of State (SOS) if required, and comply with state fees and filings.

Tax Considerations

Taxation is often the primary factor in entity selection, as it affects how profits are taxed at both federal and state levels. California imposes an annual franchise tax administered by the Franchise Tax Board (FTB), which varies by entity.

Partnerships

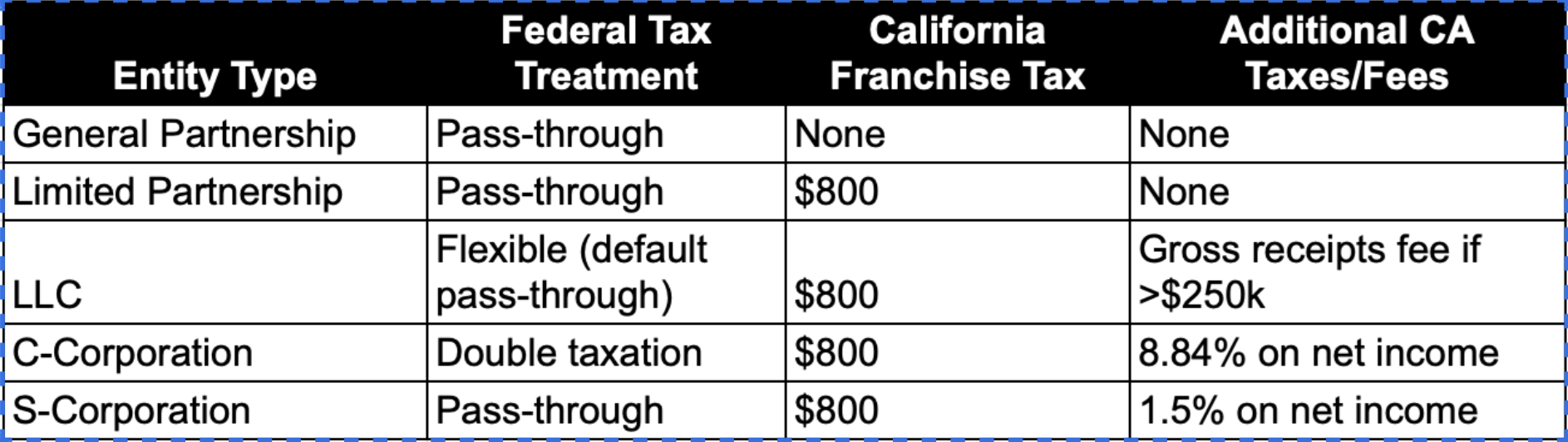

Partnerships are pass-through entities, meaning business income and losses flow directly to the partners' personal tax returns without entity-level taxation federally. Partners report their share on IRS Form 1040 and pay self-employment taxes (Social Security and Medicare) on net earnings. This can lead to higher personal tax burdens for active partners but avoids double taxation.

In California:

General partnerships do not pay the annual $800 franchise tax.

Limited partnerships must pay the $800 annual tax.

LLCs

LLCs offer the most tax flexibility. By default, single-member LLCs are taxed as disregarded entities (like sole proprietorships), while multi-member LLCs are taxed as partnerships—both pass-through structures. However, LLCs can elect to be taxed as C-corporations or S-corporations via IRS Form 8832 or 2553, allowing owners to optimize for their situation.

In California:

All LLCs pay an $800 annual franchise tax, regardless of income.

An additional LLC fee applies based on gross receipts.

If electing S-corp status, California imposes a 1.5% tax on net income..

Corporations

Corporations differ significantly based on subtype.

C-Corporations: Subject to double taxation—profits are taxed at the corporate level (21% federal + 8.84% California), and dividends to shareholders are taxed again personally.

S-Corporations: Pass-through like partnerships, avoiding corporate-level tax, but shareholders must take reasonable salaries (subject to payroll taxes), with remaining profits available as distributions (no self-employment tax).

In California:

All corporations pay the $800 annual franchise tax.

S-corporations pay an additional 1.5% on net income.

Federal and California Tax Differences by Entity Type